By Chalerm Jaitang (Prince of Songkla University)

Introduction

Access to finance is crucial for firms because it directly affects their liquidity and ability to continue operations and investment. Firms typically rely on two main sources of external financing: formal finance (such as bank credit) and informal finance (such as trade credit). Small and medium-sized enterprises (SMEs) often face greater difficulty accessing formal finance due to their lower creditworthiness compared with large or listed firms. These difficulties intensify during financial crises or macroeconomic shocks, when banks become more risk-averse and reduce lending.

In practice, many SMEs rely more heavily on trade credit than on bank loans, particularly when they lack sufficient collateral or formal credit histories. Trade credit is often easier to obtain and involves lower transaction costs than bank financing, making it an important tool for liquidity management for SMEs.

According to the 2024 Annual Report of the Office of SMEs Promotion of Thailand (OSMEP), Thai SMEs (excluding micro enterprises) accounted for 32.3 per cent of GDP and 40.6 per cent of employment [1]. These figures underscore the central role of SMEs in Thailand’s economy and highlight the importance of understanding how they manage liquidity through both formal and informal financing channels, particularly under financial constraints and during crises such as the COVID-19 pandemic.

A key question examined in this study is whether trade credit becomes more prominent during crises for firms that have access to formal finance. In this sense, the provision of trade credit during a financial crisis can act as a positive spillover mechanism, supporting other firms facing liquidity shortages.

This blog summarises some findings of my research presented at the 19th International Conference of the Thailand Econometrics Society in 2026 [2].

Data

The primary dataset is drawn from the 2021 financial statements of Thai firms obtained from the Department of Business Development (DBD) of Thailand [3]. The sample consists of 489,799 SMEs across 77 provinces, excluding natural persons.

Trade credit is measured in two dimensions:

Trade credit supply, defined as accounts receivable relative to total assets.

Trade credit demand, defined as accounts payable relative to total assets.

Formal financing access is proxied by the use of bank overdraft facilities. This measure is theoretically meaningful because overdrafts are specifically designed to smooth short-term liquidity shortages and can be adjusted rapidly in response to cash-flow fluctuations.

Key Findings

To ensure robustness, the study employs several econometric methods.

Limited access to formal finance: Only 11 per cent of Thai SMEs had access to bank overdrafts in 2021, implying constraints on formal credit during the COVID-19 pandemic.

Low use of trade credit: Median trade credit supply (accounts receivable to total assets) and demand (accounts payable to total assets) were 0.021 and 0.019, respectively. Compared with international evidence, Thai SMEs exhibit relatively low levels of trade credit usage, indicating difficulties in accessing both formal and informal finance during crisis periods.

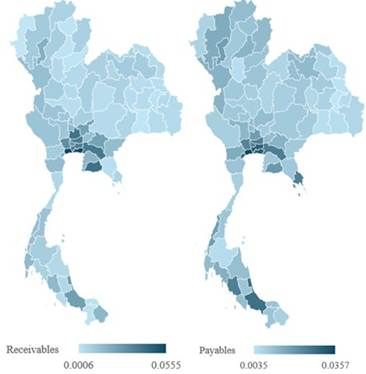

Unequal access to trade credit across firms and regions: Firm characteristics and location-based advantage matter for trade credit usage. Larger and more established SMEs, companies with foreign ownership, and firms located in Bangkok and metropolitan areas had better access to trade credit than smaller, younger, Thai-owned, and regionally located firms. The maps show that in 2021, both trade credit supply (Receivables) and trade credit demand (Payables) were more prevalent and concentrated in the capital city (Bangkok) and the metropolitan provinces than in other regions.

Formal credit supports trade credit supply: SMEs with bank overdrafts supplied more trade credit to their customers than firms without overdrafts. This indicates that formal finance enables firms to pass liquidity to other firms, generating positive spillover effects along supply chains. Therefore, formal credit complements trade credit supply.

Formal credit substitutes for trade credit demand: Firms with overdrafts relied less on trade credit from suppliers, reflecting greater financial flexibility and reduced dependence on informal borrowing. This finding supports the substitution hypothesis between formal credit and trade credit demand.

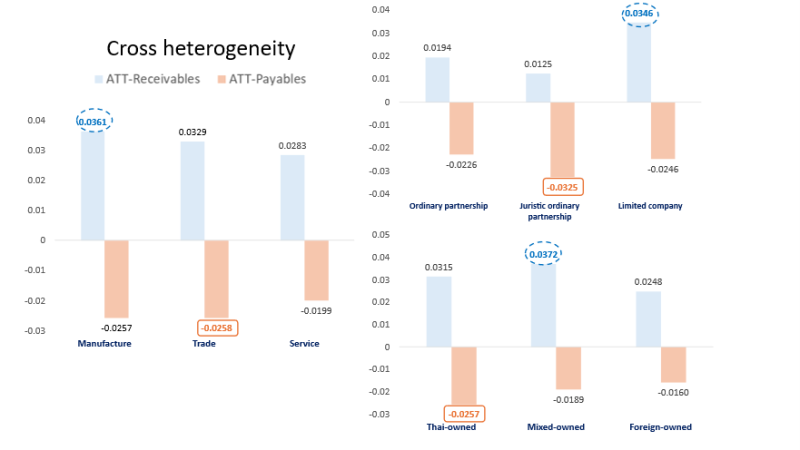

Cross-heterogeneity by firm characteristics (overdraft access): The figure shows that firms with access to bank overdraft facilities extend more trade credit supply and rely less on trade credit demand than firms without overdraft access, measured in Thai baht (THB) relative to total assets. For example, in the manufacturing sector, the difference in trade credit supply between overdraft-access firms and non-overdraft-access firms averages 0.0361 THB per 1 THB of assets, representing the largest gap across all sectors. More generally, the figure illustrates that overdraft-access firms provide more trade credit than their counterparts without overdraft access across all sectors, corporate types, and ownership structures.

Conversely, in the trading sector, the difference in trade credit demand between overdraft-access firms and non-overdraft-access firms averages -0.0258 THB per 1 THB of assets, which is the largest gap observed across sectors. The figure further indicates that overdraft-access firms rely less on trade credit from suppliers than firms without overdraft access across all firm characteristics.

What May Happen Next?

Formal and informal financing jointly determine a firm’s liquidity position. Thai SMEs face dual financing constraints: limited access to formal credit and restricted use of trade credit during financial crises. Firms experiencing both constraints are more likely to suffer financial distress and face higher bankruptcy risk (insolvency probability). When credit tightens from both channels simultaneously, liquidity shortages intensify, and vulnerability to economic shocks increases.

Implications

These findings have important implications for policymakers and SME owners, highlighting the need for effective liquidity management and diversified financing strategies. To reduce bankruptcy risk, SMEs should develop both short-run and long-run liquidity plans. In particular, young and small firms should strive to maintain good credit relationships with suppliers and financial institutions, as creditworthiness becomes especially valuable during periods of crisis. Regular assessments of trade credit risk are essential for their business.

The coexistence of limited bank credit and constrained trade credit creates a “double tightening” effect on SME liquidity. This substantially raises the risk of financial distress and bankruptcy during crises. Policy responses should therefore address both financing channels simultaneously.

From a policy perspective, initiatives that facilitate SMEs’ access to informal finance during crises, such as trade credit guarantee schemes, can help ease liquidity pressures and stabilise supply chains. Beyond crisis response, policymakers should also focus on broadening access to formal finance under normal conditions. Expanding reliable bank financing for SMEs can act as a buffer against future macroeconomic shocks (uncertainty) and financial disruptions. Special attention should be given to young, small, and regionally located SMEs, which face the greatest barriers to both bank and trade credit.

Closing Remarks

Thai SMEs face dual financing constraints when both bank credit and trade credit contract during periods of economic downturns. This double tightening significantly increases their exposure to liquidity shortages and bankruptcy risk. Policies that simultaneously strengthen access to formal finance and stabilise trade credit (informal financing) channels can enhance SME resilience, protect employment, and support economic recovery during crises.

In recent years, global uncertainty arising from political tensions, wars, and financial crises has led to repeated contractions in credit as lenders (especially financial institutions) seek to limit non-performing loans. These developments create both direct and indirect challenges for SMEs’ operations. Thus, SME owners and governments should prioritise policies that strengthen firm liquidity and resilience. Preparing for worst-case scenarios and embedding risk management into financial planning are essential steps toward sustaining SMEs in an increasingly uncertain economic environment.

[1] https://www.sme.go.th/uploads/file/20250904-175758_SME_Annual2024_Lowres_NEW.pdf

[2] https://tes.econ.cmu.ac.th/

[3] https://datawarehouse.dbd.go.th/

*The article was presented at the 19th International Conference of the Thailand Econometrics Society.