By David Suttner and Daniel Teoh (HFW)

When a company is in or near insolvency, the duties owed by directors of Australian companies under section 181 of the Corporations Act shift and directors must be mindful of creditor interests. The decision of the Supreme Court of South Australia in Ex NF Pty Ltd v Munneke examined this ‘creditor duty’, analysing when the obligation is triggered and the threshold for this shift, and contains valuable guidance for directors, creditors and liquidators.

Background: the good faith duty and creditors’ interests

The good faith duty (set out in section 181 of the Corporations Act) obliges the directors and officers of an Australian company to exercise their powers and duties in good faith, in the best interests of the company and for a proper purpose.

That duty is generally owed to shareholders.

However, when the company is in or near insolvency, the interests of the shareholders must be balanced against the emerging interests of the creditors.

Australian courts have not determined whether there should be a ‘sliding scale’ of insolvency that informs this duty (as was suggested in the 2022 decision of the Supreme Court of the United Kingdom in BTI v Sequana SA & Ors) [1] or agreed on precisely when the interests of creditors begin to override the interests of shareholders.

Australian courts have examined when this creditor-focused duty is triggered, referring variously to:

“an insolvency context” [2]

“doubtful solvency” [3]

“a financial state short of actual solvency” [4]

“financial instability” and the company’s directors “should have been concerned for [solvency]” [5]

Perhaps the Western Australian Court of Appeal put it best in Westpac Banking Corporation v Bell Group Ltd (No 3) (in liq) when it stated that the ‘creditor duty’ arises when there is “a real risk that the creditors of a company in an insolvency context would suffer significant prejudice” [6].

The question therefore remained, when and in what context are directors of Australian companies required to consider creditors’ interests?

The decision in Ex NF Pty Ltd (in Liq) v Munneke

The Supreme Court of South Australia (Supreme Court) considered this question in Ex NF Pty Ltd (in liq) v Munneke [7] (Munneke).

In 2014, company funds were used to acquire cryptocurrency, which later appreciated in value. In 2015 and 2018, those cryptocurrency investments were redeemed and used to purchase real estate.

The Supreme Court held that, at the time of the real estate purchases, there was a “real and not remote risk of insolvency” as the company had accrued significant Australian Tax Office debts of over $2.23 million (including GST and income tax) at the time of the acquisition(s). While the existence of tax liabilities did not constitute a breach of duty, they showed that the company was in the “zone of insolvency”, which had shifted the focus of a director’s good faith duty from shareholders towards creditors.

Mr Munneke, the director of Ex NF Pty Ltd, (Director) was criticised for not properly informing himself as to the company’s financial position. Considering the extent of the company’s tax liabilities, a reasonable director would not have paid company funds away and prejudiced the company’s ability to pay its creditors. Accordingly, the Director had breached (amongst other things) his duty to act in good faith in the interests of the company.

The decision is in line with other Australian judgments in which the courts have held that, in certain circumstances, directors can be found to have breached the duty of good faith by failing to take the creditors’ interests into account, even while the company was solvent. That was the outcome in Termite Resources [8], in which the company made distributions when it was neither insolvent nor near insolvency. Indeed, the iron ore price (a key factor in that case due to the nature of the company’s business) remained high when the distributions were made. Nevertheless, the court held that the payments were made in breach of the directors’ duty to creditors: the directors were placing the creditors in jeopardy because a drop in iron ore prices could put the company at risk of being unable to pay its long term liabilities.

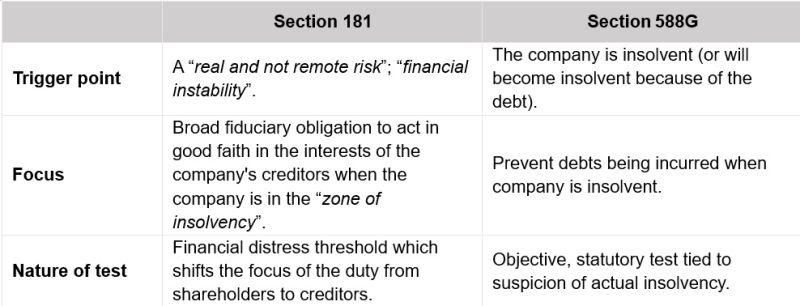

Insolvent Trading Duty

Section 588G of the Corporations Act obliges directors of Australian companies to prevent insolvent trading (Insolvent Trading Duty). To establish breach of the Insolvent Trading Duty, a three-part test must be satisfied:

The company incurs a debt;

The company is insolvent at that time or becomes insolvent because of the debt; and

There were reasonable grounds to suspect insolvency at the time in question.

The Insolvent Trading Duty is triggered by actual insolvency, not mere financial difficulty or the risk of insolvency and this statutory test requires directors (and the courts) to consider whether a reasonable person would suspect insolvency, not whether insolvency is “near” or a “real and not remote risk.”

Two duties: a comparison

The table below sets out the key differences between the two duties:

Arguably, there is more risk of a director breaching the ‘creditor duty’ than the Insolvent Trading duty. The threshold is lower: actual insolvency is not required. The window of risk starts earlier because a mere prospect of insolvency can trigger the ‘creditor duty’, whereas actual insolvency is required under section 588G.

It is important that directors are aware of this distinction, particularly because no ‘safe harbour’ defence is available for a claim arising out of breach of the ‘creditor duty’ under section 181. (Of course, it is unlikely a director who breached the ‘creditor duty’ would be able to meet the strict requirements of safe harbour).

Commentary

The Supreme Court’s decision in Ex NF Pty Ltd v Munneke and the other judgments discussed in this article provide valuable guidance for directors of Australian companies:

Appraise yourself of the company’s finances (e.g. income, debt and cash flow). This is not a one-off task: markets change, prices move and the company’s business may develop.

Familiarise yourself with known debts which are due and owing (e.g. payroll tax) and the company’s future and / or contingent liabilities.

If the board is considering making a payment which is out of the ordinary course of business, acquiring an asset or distributing profits, this transaction should be scrutinised with the company’s solvency in mind.

The Australian courts have not settled on a specific test, timeline or other yardstick by which directors can evaluate whether they owe the duty of good faith under section 181 to the shareholders (as normal) or the duty has shifted to the creditors. Given the risk of inadvertently breaching the ‘creditor duty’, prudent directors would take a conservative approach if the company is nearing or at risk of insolvency.

The steps that directors must take to satisfy their duty to creditors under section 181 will vary. Much will depend on the according to the circumstances. The factors that the court will, it appears, consider include:

the number, type and the amount owed to each creditor;

the company’s financial situation. Even though the ‘sliding scale’ approach suggested by the Supreme Court of the United Kingdom has not been uniformly endorsed by courts in Australia, it is clear that more weight should be given to creditors’ interests the closer the company’ comes to insolvency;

whether the company is part of a corporate group:

in the Bell Group Ltd liquidation, the company was part of a large corporate group. This meant that the directors faced a more complex task when considering the interests of creditors and more work was therefore expected of them.

Holding companies should be wary of being treated as de facto directors of subsidiaries for breach of director duty claims; and

Whether directors conducted a fulsome analysis of the impact of any transactions.

Boards should not focus only on potential insolvent trading in situations of financial distress, but should stay alive to the potential (earlier in time) exposure to liability under section 181.

Whether directors owe duties to creditors – and when those duties arise – is an important question and one which courts in other jurisdictions have grappled with. The ECSC Court of Appeal decision in Byers v Chen [9] (in which HFW are acting) deals with the position under BVI law and you can read HFW's article on that decision here.

*This article was originally published by HFW. You can view the original article on HFW's website here.

© 2026 Holman Fenwick Willan LLP. All rights reserved.

Whilst every care has been taken to ensure the accuracy of this information at the time of publication, the information is intended as guidance only. It should not be considered as legal advice.

[1] [2022] UKSC 25.

[2] Kinsela v Russel Kinsela Pty Ltd (in liq) (1986) 4 NSWLR 722 at 732.

[3] Nicholson v Permakraft (NZ) Ltd (in liq) [1985] 1 NZLR 242 at 249.

[4] The Bell Group Ltd (in liq) v Westpac Banking Corp (No 9) (2008) 39 WAR 1, 540 [4445] (Bell Group Ltd).

[5] Linton v Telnet Pty Ltd (1999) 30 ACSR 465 at 471, 478.

[6] (2012) 44 WAR 1, 358 [2046].

[7] [2025] SA SC 165.

[8] Termite Resources NL (in liq) v Meadows, in the matter of Termite Resources NL (in liq) (No 2) [2019] FCA 354.

[9] Byers & Richardson (as Joint Liquidators of Pioneer Freight Futures Company Limited) v Chen Ningning (BVIHCMAP2024/0009).