Non-Financial Liabilities and Effective Corporate Restructuring

By Bo Becker (Stockholm School of Economics) and Jens Josephson (Stockholm Business School)

The system for managing corporate insolvency varies in fundamental ways between countries, with important effects on economic outcomes. Chapter 11 of the US Bankruptcy Code forms the legal basis of the successful American regime, which can handle distress in a formal process without liquidating assets, closing businesses, and with limited job losses. Many countries aim to replicate key features of Chapter 11, such as a broad automatic stay on creditor action and senior financing during the reorganization. However, this reform process is slow and complicated, and has not, in our view, been generally successful. For example, the fact that large European firms still use the US system suggests that European reforms have some way to go.

In a new working paper, we propose that non-financial obligations pose an important challenge in many systems, and that this may be a key component for replicating Chapter 11’s success elsewhere. Our starting point is that just as high financial obligations can impede the successful operation of a firm, non-financial obligations can impede the continued operation of a viable business. Non-financial obligations—including under office or equipment leases and under long-term supply and service contracts—are often large. Ayotte (2015) reports that lease obligations constitute twenty-three percent of liabilities in a sample of large Chapter 11 cases, and 71 percent of liabilities at the 90th percentile.

In Chapter 11, a key mechanism for managing operating liabilities is the right to reject executory contracts. An executory contract is one where both parties have remaining obligations (one-off transactions do not create executory contracts). Examples of executory contracts are office leases, where the landlord will supply an office and the tenant lease payments, long-term vendor contracts, and licensing agreements. Under Section 365 of Chapter 11, executory contracts can be rejected (abandoned), assumed (retained), or assigned (transferred to a third party). This gives firms considerable ability to reduce their future obligations. Examples of bankruptcy cases where this was important include Kmart in 2002 and Hertz in 2020. For Kmart, the number of leases was large and time short, and the company sold rejection rights to a third party (Gilson and Abbott, 2009). For Hertz, which at the time of its Chapter 11 process leased almost half a million vehicles under a ‘master lease agreement’, a key issue was rejecting part of the leases, and the firm argued that these were separate contracts (in the end, Hertz was allowed to retain some vehicles). These cases highlight the important option values embedded in the right to reject a contract. In a recent Chapter 11 process, WeWork apparently plans both to reject a large number of executory contracts (mostly office building leases) and to renegotiate others.

Modelling the Treatment of Executory Contracts

Outside of the US, it remains rare for restructuring law to explicitly involve operational claims the way Chapter 11 does, and especially to give such unconstrained rights to the debtor company to reject contracts as part of a non-liquidating process. It is more common that other jurisdictions have a system for the treatment of executory contracts in a liquidating process (similar to Chapter 7), which matters for the sharing of liquidating values but not for the question of whether a firm survives. In other words, most countries do not allow reduction of executory contract obligations for firms that will continue as a going concern. We develop a model of an insolvent firm with financial and operational obligations, and study how capital structure and insolvency choices depend on whether debtors may reject executory contracts. We characterize outcomes under a restructuring process which allows adjusting both types of obligations (Chapter 11) and one limited to financial claims (most other processes) and also consider a setting without restructuring possibilities.

In the model, restructuring operations in bankruptcy differs from (re)negotiating because the bankrupt firm may reject contracts. This reduces operating liabilities in Chapter 11, alongside financial debts. Putting all liabilities on the table raises the likelihood of successful restructuring. When both operational and financial claims are addressed simultaneously, it is more likely that firm liabilities can be sufficiently reduced for the businesses to survive, and as a result, fewer firms are liquidated.

The model connects the rejection of executory contracts to capital structure and restructuring outcomes. Predictions about inefficient liquidation are difficult to test because they will tend to be ‘off the equilibrium path’, i.e., insolvent firms will renegotiate out of court, or firms may take on less debt to reduce the risk of distress in the first place. We therefore focus our tests on capital structure: when executory contracts can be rejected, financial leverage should be higher (because distress is less damaging). Testing this cross-country is probably not reasonable—there are too many institutional differences. Therefore, we focus on a difference-in-difference test. We sort industries based on the use of executory contracts. This can be estimated from rent and lease payments reported for US firms, and we assume that the same industries rely on executory contracts everywhere. The Fama-French (30) industries most reliant on executory contracts are Retail; Restaurants, Hotels and Motels; Communication; and Personal and Business Services. In Retail, we estimate that the median listed US firm has such obligations (under what would be executory contracts if they filed for bankruptcy today) worth around a third of book value of assets. Industries with low reliance on executory contracts include Finance; several manufacturing industries; Mining; and Chemicals.

Empirical Tests Suggest Large Effects

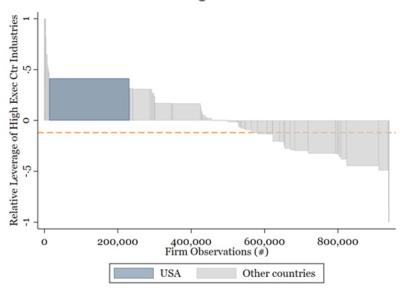

We test the prediction that a rejection option encourages leverage by comparing the leverage of industries with high and low executory contract use. We compare the US (where rejection is relatively easy) to everywhere else (where it is impossible, cumbersome, or limited), controlling for fixed effects for year-country and for year-industry. We find large and statistically significant positive effects on leverage. In cross-country tests, we estimate that a change in the ratio of executory contracts from the 25th to the 75th percentile (around 4 percent of annual revenues) corresponds to an increase of leverage in the US of 0.02 (average leverage is 0.231), or around 10% higher debt. Below, we replicate Figure 1 from the paper, which highlights the variation across countries in leverage of leverage in high executory contract industries. The US stands out compared to average, and apart from a few small countries with very few observations, as the highest leverage in these industries.

Figure 1 from the paper. Each bar is a country coefficient, with width equal to the number of firm-year observations in our sample. The orange line indicates the non-US average.

We provide two further tests of the leverage hypothesis. First, we compare Israeli firms before and after a new Company Law was introduced in 2019, allowing US-style unconditional rejection of contracts. The Israeli before and after tests produce similar magnitude estimates. We are currently looking for other examples of similar reforms.

Finally, we also test the model's prediction in lending data (from Dealscan). This offers a separate take from the stock data (leverage) and offers additional variables such as the price of credit. We find that high executory contract industries are associated with higher credit volumes in the US, as well as lower prices (spreads). This confirms that effective operational restructuring increases the debt capacity of US firms.

All the evidence, taken together, suggests that executory contracts matter for financial leverage—the financial debt capacity of firms in industries that rely on executory contracts is significantly affected by a rejection option. This evidence is consistent with our model, which highlights how rejection can avoid liquidation and improve debt capacity. Importantly, the Israeli example suggests that reform in the US direction is possible in other countries and can be effective outside of the particular institutional setting of Chapter 11. Other countries may be able to similarly implement rejection options.

* The full paper may be found here.

* A version of this post was first published on The FinReg Blog, and subsequently reposted on the Oxford Business Law Blog.